Make / Model Search

News - Market Insight - Market Insight 2023Market Insight: July supply and demandAds, discounts drive July sales for some brands, ship literally comes in for others14 Aug 2023 By NEIL DOWLING DEMAND for new cars in the historically buoyant month of June spilled over into July and while not matching the pace of the last month of the previous financial year, the seventh month produced some strong individual sales figures.

July posted a total vehicle sales figure of 96,859, down 22.5 per cent on the especially strong June result of 124,926 units that was spurred by some tax bonuses, as well as a continuation June’s aggressive advertising and discounting by some OEMs – for the first time since the pandemic – encouraging consumers to purchase in-stock or soon-to-arrive vehicles.

Most OEMs did well in July, despite the overall slide in sales.

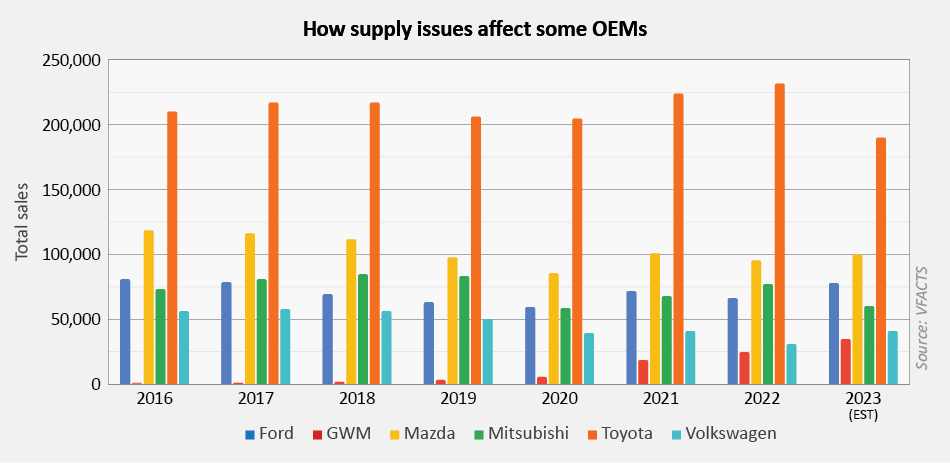

Toyota, once the brand with more than 22 per cent of the Australian market, is starting to slowly regain lost ground. Its market share is up to 19.8 per cent for July from June’s 15.9 per cent as its ships literally came in.

Ahead is still the task of filling a lot of backorders caused by production interruptions and shipping bottlenecks.

On a year-to-date (YTD) basis, Toyota has a 16.4 per cent market share and, for the month of July, 19.8 per cent (down from 23,2 per cent in July 2022).

Its slump is the worst of all OEMs, with the closest decline recorded by Mitsubishi at 2.45 per cent down on the previous year’s same seven-month period.

Toyota’s sales for the seven months of the 2023 year are down 20.9 per cent (compared with the same time in 2022) and, for the month, 1.9 per cent down from July 2022.

More upbeat is the situation at Mazda. In July it retained second spot on the OEM ladder with 8307 sales (Japanese compatriot Toyota was first with 19,191 units) and a market share YTD of 8.7 per cent, around the same as in calendar year 2022.

Mazda’s 8307 sales for July were up 5.4 per cent on the same month in 2022, while YTD sales are up 1.6 per cent.

Last month Mazda was up about 500 units on third-placed Hyundai (and up 12,717 sales YTD) while in July, Mazda moved ahead (and/or Hyundai slipped) by 1786 units (and a difference of 14,503 YTD).

Pitcher Partners said that this was attributed to Mazda’s abundant supply in comparison to the tight flow of Hyundai products.

In other OEMs, Ford sales powered ahead in July with a 60.1 per cent jump in July compared with July 2022, and a 37.2 per cent leap YTD. Its YTD market share is 6.7 per cent but its big gain in July pushed that month’s market share to 7.3 per cent.

Ford sales are driven by growing inventories and dealer stocks on an easing in supply chain issues. The OEM remains strongly dependent on the Ranger ute (YTD up 35.6 per cent for the 4x4 and up 96.3 per cent for the 4x2) as the model contributed 70.4 per cent of all Ford units sold YTD, and 72.3 per cent in July.

Much of Ford’s remaining sales are attributed to the Ranger-based Everest large SUV. In July, its sales were up 88 per cent on July 2022 and on a YTD basis, up 23.4 per cent.

Popularity of the Everest was responsible for 18.1 per cent of Ford sales in July and 15.3 per cent of its YTD sales.

MG had a great June and a strong July. In July, sales were up 77.2 per cent on the same month in 2022 and YTD, up 16.4 per cent.

The Chinese-owned historic British brand now has a YTD market share of 4.7 per cent and in July, thanks to some aggressive marketing, had a 5.5 per cent share.

Interesting to note that MG’s ZS SUV had 3852 unit sales in July, outpacing the Toyota RAV4 with 2750 sales. YTD, the ZS found 17,431 new owners while the supply-affected RAV4 sold more than 100 units less at 16,273.

Mitsubishi continues to take hits. In July, it was down 26.2 per cent monthly and is 26.1 per cent behind in YTD terms.

The Japanese OEM hasn’t seemed to have major problems with supply but still has negative sales in all models except Outlander which is up 35.7 per cent for July and 24.3 per cent YTD.

In July, Mitsubishi had a 5.2 per cent market share YTD and 4.3 per cent for the month of July. The new-generation Triton ute likely cannot come soon enough.

Volkswagen is on a big roll. July showed sales are up 46.8 per cent compared with the same month in 2022, while YTD sales are up 58.8 per cent at 23,938 units.

It lifted market share to 3.5 per cent for the YTD, up 1.1 per cent compared to the same seven months of 2022. For July, the German brand’s 3.1 per cent share was up 0.67 per cent on the same month last year.

Also steaming ahead is GWM. In June it had a 59.7 per cent increase in monthly sales and repeated that in July, with YTD sales up 88.2 per cent to 20,112 units, and July sales up 20.5 per cent on the same month in 2022.

It has a YTD market share of 3.0 per cent – overtaking Nissan which is on 2.9 per cent – and in July, its share on the market was 2.6 per cent.

GWM vehicles come at an accessible price, and the Chinese brand has been offering a discount on almost all vehicles for $1000-$2000.  |

Click to shareMarket Insight articlesResearch Market Insight Motor industry news GoAutoNews is Australia’s number one automotive industry journal covering the latest news, future and new model releases, market trends, industry personnel movements, and international events. |

{kind=link}

Connect with us

Facebook Twitter Instagram