Make / Model Search

News - Market Insight - Market Insight 2022Market Insight: Mazda, Kia fill Holden legacyMarket moves: Without a strong SUV and ute presence, Holden would have struggled if it remained in Australia, whereas Mazda keeps adding to its SUV portfolio (CX-60 pictured). Toyota a beneficiary of Holden’s shutdown but Mazda and Kia have taken Lion’s share Gallery Click to see larger images 12 Dec 2022 By NEIL DOWLING IT HAS been five years since Holden pulled stumps on Australian manufacturing and its brand was axed by GM at the end of 2020, wiping its name from the automotive shopping list and threatening to dilute a foundation enterprise that served generations.

Holden’s legacy is now parked at car shows attended by enthusiasts and an occasional – surprising given the number of cars it made – appearance on our roads.

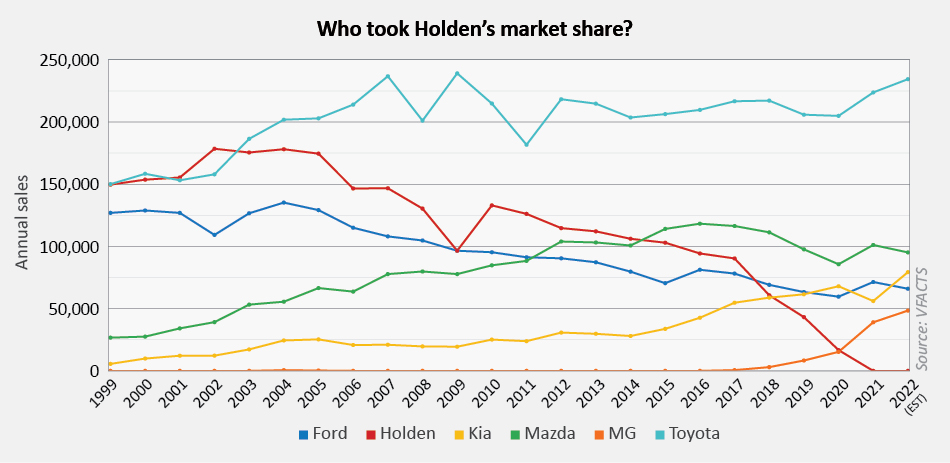

In 2002, Australians bought 824,309 new vehicles, of which Holden had a 21.6 per cent stake, selling 178,392 cars.

Incidentally, Toyota (which had a 19.2 per cent stake of the market in 2002) now has that same 21.6 per cent share in the year-to-date November sales.

Where Ford had a 2002 market share of 13.2 per cent, Mitsubishi came in third with 8.2 per cent and the rest of the 55 brands were each in the sub-5.0 per cent bracket.

Holden does not appear on the 2022 VFACTS sales list, while Ford has a 6.1 per cent share, Mitsubishi has 7.3 per cent and both are beaten by Mazda with 8.8 per cent.

There are 54 brands listed (some are doubled up, for example Mercedes-Benz Cars and Vans; Fiat and Fiat Professional) and, year-to-date, sales are 993,509 units with estimates to end the year at about 1,084,000.

Which car brands now fill that 21.6 per cent stake held by Holden in 2002?

Toyota still fills the bulk of the loss of Holden but there’s some brands that barely raised an eyebrow back in 2002 that are performing strongly.

Kia sold 5603 cars in 1999 for 0.8 per cent of the market and few would have put money on this brand achieving much for the future, especially up against the industry leaders.

But four years later, Kia sold 17,235 units and except for the 2008-09 period when the Global Financial Crisis bit into the economy and affected all car-makers, has been on a strong improvement each year.

For 2022, it is expected to sell about 79,500 vehicles for a market share of about 7.5 per cent, greater than Mitsubishi, Ford and Hyundai.

Mazda has lifted its share of the market from 3.4 per cent in 1999 to 5.8 per cent in 2002 (directly attributed to the launch of its Tribute SUV), then to 6.7 per cent in 2005 and 9.3 per cent in 2012, to 9.7 per cent in 2018 and currently about 8.8 per cent.

Despite its market share slipping to 8.8 per cent this year (to date November) compared with 9.7 per cent last year, Mazda is the second most popular brand in Australia after Toyota.

The difference has been taken up by growth at Kia (7.3 per cent now up from 6.3 per cent in the previous corresponding period) and MG (4.5 per cent now, 3.7 last year), Mitsubishi (7.3 per cent now, 6.4 then).

Aside from the lack of a major player such as Holden, the boost to these three comes at the cost of percentage drops at Nissan which has fallen to 2.4 per cent in the 11 months of this year compared with 4.0 per cent last year; Ford (now 6.1 per cent from 6.8 last year); and Volkswagen that has fallen to a market share of 2.8 per cent from 3.9 per cent last year.

Much of these falls has been caused by the ongoing erosion caused by COVID-19 on a large slice of the supply chain, from raw materials to logistics through to production and retailing.

Volkswagen, for example, has its sales slashed by 27.2 per cent this year compared with 2021 as the supply of its vehicles is choked by production holdups, while Skoda is down 32.4 per cent and Audi by 10.5 per cent.

The dynamics of the Australian market have also changed since 1999. Holden’s Commodore was 55 per cent of its brand sales in that year, while its SUVs (Captiva, Suburban, Jackaroo and Frontera) represented 3.8 per cent and utes (Rodeo and Commodore Ute) contributed 17.5 per cent.

By 2015, close to the end of its market presence, Holden’s Commodore contributed 27 per cent to the brand while its SUVs (Captiva 5, Captiva 7 and Colorado 7) were 18.4 per cent of the total and its utes (Commodore Ute, Colorado 2WD and 4WD) represented 22.8 per cent.

Clearly if Holden had remained, its strength would be gauged on its presence in the SUV and ute sectors.  |

Click to shareMarket Insight articlesResearch Market Insight Motor industry news GoAutoNews is Australia’s number one automotive industry journal covering the latest news, future and new model releases, market trends, industry personnel movements, and international events. Car Finance |

Connect with us

Facebook Twitter Instagram