The power of petrol

BY TERRY MARTIN | 7th Dec 2010

As evidenced by the Skoda Superb’s win in this year’s large-car section, however, ‘Best Cars’ is no indication of a car’s popularity in the marketplace – or what most buyers consider to be the best car for them, as reflected by actual vehicle sales.

Whereas Skoda has managed 321 sales so far this year for the Superb, for example, Holden has sold more than 42,000 Commodores – yet that was not enough to see the updated VE Series II make the finals in its category, let alone claim the winner’s trophy and the marketing kudos that comes with it.

Another interesting point with this year’s awards was that nine of the 15 category winners were diesels, spanning light cars, small cars, medium cars, large cars and SUVs.

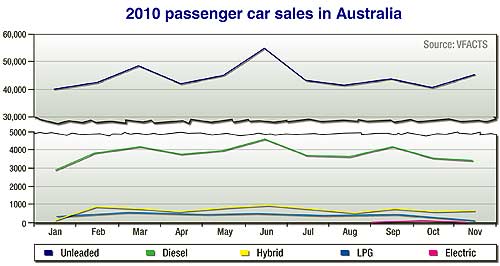

But to what extent ARE diesel cars growing in popularity? Such a high number of award winners with diesel power sparked Market Insight’s attention as the Federal Chamber of Automotive Industries last week released its latest VFACTS figures, which showed that diesel cars accounted for just 7.0 per cent of Australia’s passenger car market in November, compared to 91.2 per cent for those running on petrol.

There is no doubt that diesel sales have climbed as the new-vehicle market has returned to form and, likewise, it is impossible to overlook the increasing number of diesel engine options across model ranges – particularly those from luxury brands – available in Australia.

But despite their improved refinement, efficiency, performance and suitability to local conditions generally, diesel sales growth in Australia is continuing to occur slowly.

During the course of this year the popularity of diesel power has remained on a relatively even keel when viewed as a percentage of ‘fuel type’ (which as well as petrol includes hybrid, LPG and now electricity), rather than in comparison to last year when the industry was still recovering from the economic downturn.

Over the course of this year, diesel’s monthly share in passenger car sales in Australia has fluctuated from a low of 6.7 per cent to 8.4 per cent, compared to petrol sales ranging from 89 to 92.1 per cent.

While figures released this week show the share of diesel in the British new-car market in 2010 year-to-date at 45.8 per cent – up more than four per cent – and petrol at 53 per cent, the diesel-versus-petrol YTD share in Australia is currently at 7.7 versus 90 per cent.

Australia has recorded 486,939 petrol car sales YTD, compared to 41,660 diesel, 7576 hybrid, 4796 LPG and 112 electric cars.

For diesel, that is around 5000 units ahead of the full 12 months of 2009, and is streets ahead of the 27,050 diesel car sales recorded in 2007 – the last time Australia’s new-vehicle market passed one million units.

Back then, diesel accounted for just 4.2 per cent of new-car sales, compared to petrol on 93.9 per cent (597,896 units).

Over the following two years, which saw overall passenger car sales fall around 40,000 units in 2008 and a further 56,000 in 2009, diesel’s share climbed to 6.0 per cent in 2008 (on 36,138 units) while petrol lost ground to 91.9 per cent (with sales down almost 50,000 units).

Last year, both petrol and diesel’s share of the overall passenger car market was fairly steady – 6.8 per cent for diesel (36,632 units) and 91.4 per cent for petrol (despite a further 53,800 sales fall to 494,211 units).

In 2010 YTD, diesel’s one percentage point climb in market share is part of a continuing trend, but cannot match the higher levels of growth recorded in the UK.

Over there, diesel has experienced steady annual growth of around two per cent, with some particularly strong surges in recent years, including a 4.3 per cent climb in 2005 (to 36.8 per cent), a 3.4 per cent jump in 2008 (to 43.6 per cent) and, after a drop last year to 41.7 per cent, a strong upswing of 4.2 per cent in 2010 YTD.

If those sorts of figures in percentage terms translated to the Australian passenger car market, diesel’s influence could begin to weigh heavily on petrol and force more manufacturers into the game, particularly those from Japan who continue to overwhelmingly favour petrol power.

But with our relatively high cost of diesel and historically low price of petrol, there is little incentive for change from either car companies or consumers.

The question is often asked why diesel is cheaper than petrol in the UK and Europe compared to Australia.

There are a host of reasons, but certain tax regimes favour diesel fuel and the greater demand and market share of diesel passenger cars in Europe provide economies of scale and exert price competition that lowers diesel prices.

In Australia, there is far less competitive pressure on diesel prices because, as outlined here, diesel represents only a fraction of total passenger car sales.

This could change if sales of diesel cars continue to increase – and if the Australian appetite for SUV/4WDs continues, which is a completely different situation when it comes to diesel market share.

In stark comparison to passenger cars, diesel SUVs currently account for around a third of all sales in this segment.

While it has always enjoyed a relatively strong following – accounting for 21 per cent back in 2006, with 35,847 units, for example – its rise in percentage terms has been remarkable, and almost exclusively at the expense of petrol SUVs.

Whereas petrol SUVs held a 78.9 per cent share four years ago (on 134,812 sales), petrol’s domination has consistently eroded to be at 69 per cent last year (on 129,903 sales) and YTD in 2010 has fallen further to 65.5 per cent (despite volume rising to 142,000).

By comparison, diesel SUV sales have doubled over the same timeframe and its share has climbed 13.1 per cent.

Diesel’s share went to 23.8 per cent in 2007 (on 47,153 sales), rising to 28.7 per cent in 2008 (on 55,804) and, after the GFC limited growth to 1.9 per cent last year (on 57,556 units), oil-burning SUVs have returned to form this year, up to 34.1 per cent YTD on 73,853 units.

Both luxury and mainstream marques can take credit for this share improvement, and significant new models such as Ford’s Territory diesel will help fuel further growth in 2011.

For the overall passenger car market, though, there is little to indicate that the continued influx of new models – or publicity from award recipients, for that matter – will do anything more than continue with modest growth.

Indeed, hybrid vehicle sales, which have started to improve with the Camry Hybrid this year and should now ramp up with cheaper new models such as Honda’s Insight, could eat away at the gains diesel has made.

It remains to be seen whether the ‘Best Cars’ program will continue to rate diesel ahead of petrol and/or hybrid across most vehicle categories in Australia.

But with the ‘People’s Choice’ award – the one made by those driving out of showrooms in a new vehicle – the sales trends clearly show that petrol power is set to dominate for many years to come.