French connections

BY TERRY MARTIN | 26th Oct 2009

Indeed, while Renault, Peugeot and Citroen have all experienced modest sales growth as the new-vehicle market has expanded – Peugeot performing best – the three French marques have experienced downturns this year that run much deeper than the industry-wide decline of 13.1 per cent.

Peugeot and Renault are down at least 20 per cent, the latter off a low base, while Citroen has fallen twice that rate year-to-date (YTD).

This is a test of brand strength and consumer acceptance as much as other factors such as model range, exchange rates, vehicle allocations, marketing budgets, retail presence, resale value and so much more.

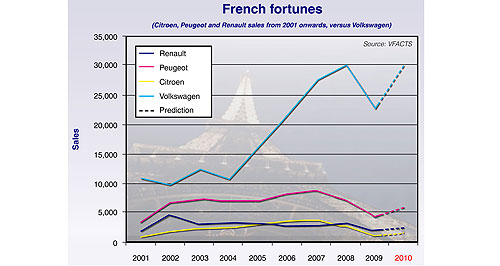

And the how the French have fared makes interesting reading alongside one of the benchmark mainstream European brands: Volkswagen.

Citroen might well have come out from the cold over the past decade with its new breed of small cars, eschewing the quirkiness the marque once held dear for mainstream acceptance, but it has not managed 4000 sales in a calendar year, even in the recent boom.

A small range, limited sales and marketing resources and, at times, insufficient vehicle allocations mean that Citroen’s sales – and, by extension, its brand and product awareness – are still low compared to rival manufacturers, such as its compatriot Peugeot.

Importer Ateco Automotive has described Citroen’s growth as “organic”, based upon a deliberate strategy of letting its share grow naturally rather than over-pushing it in the market. It points to “sustained growth, stable growth” that does not stop the moment marketing dollars are switched off.

Accordingly, Citroen achieved useful growth in the pre-GFC period, but in times of economic downturn its sales have plummeted – down a massive 41.7 per cent YTD.

In 2004, Ateco was targeting one per cent of the Australian new-vehicle market with Citroen, or around 8500 units. Based on its current running rate, Citroen could end the year with less than 1700 sales, taking it back to 2002 levels. Its retail share YTD is 0.2 per cent.

Peugeot, which is distributed through a different independent operation, Sime Darby, has set itself similar targets to its sister brand Citroen – and has come much closer, with 0.8 per cent of the market in 2006/2007 and sales in 2007 exceeding 8800. It has slipped since then, but should still reach around 6000 sales this year, holding on to about 0.7 per cent share.

Desirable small cars and concentrated marketing efforts have had a positive influence on Peugeot’s Australian growth chart. Unlike Renault and Citroen, Peugeot’s Australian vehicle allocations have also been sufficient for most model lines, and the move to position itself as a specialist in diesel power seems to have worked.

It benefits from being the more mainstream brand in the PSA Peugeot-Citroen partnership, and the strength of the European lion badge remains high in Australia.

Peugeot (and Citroen, for that matter) has grown its brand Down Under on the back of product rather than wild marketing campaigns that have seen sales fluctuate at other marques – and it will be new models, such as more commercial vehicles and a long-overdue small SUV, that bring it more success in the future.

GoAuto has written much about factory-backed Renault’s sales performance since it made a grand return to Australia in 2001, armed with a $60 million establishment budget and some exciting, innovative and albeit niche-appeal cars including the Clio Renault Sport and Megane Scenic.

The arrival of new models has been slow, stifling growth and, in earlier times, forcing marketing funds to be funnelled into limited-volume cars. Vehicle allocations, specification restrictions and, in the case of the Megane hatchback, a polarising design, have also hurt.

Renault is down 20.4 per cent YTD and might not make 2500 sales for the full year – a result that would be its worst since the brand returned to Australia. Back in 2001, the previous management was expecting 10,000 annual sales by 2004 and no less than 25,000 come 2007.

The company is no longer overplaying the Renault brand’s possibilities in Australia and has set about achieving incremental growth with more competitive vehicles, such as the competent Koleos compact SUV, which can be sourced from low-cost countries rather than Western Europe.

For all three French brands, the factory-run Volkswagen remains a benchmark that deserves close consideration. VW is an established and accepted brand in Australia, with a broad palette of vehicles, some standout performers – Golf has established a huge following, holding its own as newer rivals have entered the field – and solid resale values.

Take a good, long look at VW’s enviable chart. Its sales growth is all the more impressive when one considers that it is down a mere 5.4 per cent YTD and looks like reaching 30,000 sales come December 31 – ahead of where it was 12 months earlier.

Can the French brands ever reach this sort of level? Renault management once believed it possible, but it looks a distant mark for all three French brands. Achieving a third of VW’s sales is a more realistic target, with new models in popular segments perhaps making all the difference.