Make / Model Search

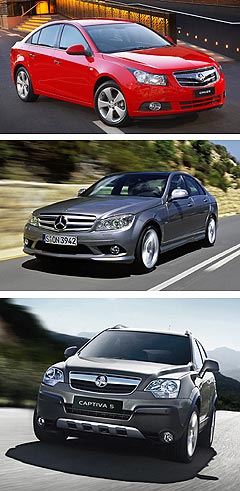

News - VFACTS - Sales 2010 - JuneJune VFACTS: Biggest sales month in historyTop performer: Holden's Commodore remains Australia's top-selling car, even though its sales dipped in June. FCAI says million vehicle sales unlikely in 2010, despite record June sales5 Jul 2010 AUSTRALIANS bought more new vehicles in June than in any month in history, yet at the halfway mark of 2010, the nation’s peak automotive industry body expects total 2010 sales to fall well short of the million-plus record set in 2007. According to official VFACTS statistics released today by the Federal Chamber of Automotive Industries (FCAI), June new-vehicle sales were up 5.7 per cent or 5875 vehicles on the same month last year at 108,722, eclipsing the previous best June sales figure of about 106,000 in June 2008. The boom June sales result, driven by the large-scale return of private buyers to the market and the usual end-of-financial-year business vehicle purchases, brings the year-to-date 2010 sales tally to 531,168 – up 16.7 per cent on the first six months of 2009. For only the third time in history, more than one million new vehicles were sold in the 2009/10 financial year (1,013,273), and the industry continues to bubble along at an annualised running rate well over one million vehicle sales. As a result, the FCAI has raised its full-year industry forecast from 940,000 to “in excess of 980,000”, which would be well up on the 937,328 vehicles sold last year but significantly short of million-plus records achieved in 2008 (1,012,164) and 2007 (1,049,982). The FCAI says the increased numbers of private buyers across all sales segments is a clear demonstration of renewed confidence in the marketplace after last year’s global financial crisis-led slump. However, it remains cautious of stalling business vehicle sales in the wake of the federal government’s small business tax incentives. The FCAI believes the full effect of recent and (and future) official interest rate rises on private vehicle sales remains to be seen and, although it admits its forecast is more conservative than the million-plus estimates held by many observers and car companies, it says other factors could also dampen new-vehicle demand. “I think we are being conservative in our forecast,” said FCAI chief executive Andrew McKellar. “There’s no denying that if you look over the six or nine months the market has been performing pretty much consistently at an annualised rate of more than a million. “We have upgraded our forecast in June and that’s based on the performance of the market year-to-date. I think there are probably still one or two factors out there that we just want to be measured about. “They include waiting a little further to make an assessment of the impact interest rate increases will have. We’re yet to see that filtering though to have any real impact on the market, but we’re just being a little cautious because of that factor.  From top: Holden Cruze, Mercedes-Benz C-class, Holden Captiva. From top: Holden Cruze, Mercedes-Benz C-class, Holden Captiva.“Equally, we want to make a further assessment about what’s occurring in other international markets, in particular having seen some of the volatility that is arising in some of the European financial markets and whether or not that will have any impact on the real economy. “Of course, the other factor out there is whether or not there is any flow on from the timing of the forthcoming federal election. It shouldn’t be a big factor – there’s no fundamental reason for it to halt people’s spending – but nonetheless past practice indicates that elections can cause people to divert for a period. “There’s no doubt it’s a judgement call and arguably we could have gone stronger and I think many industry analysts are doing so, but at this stage we just want to be measured in our outlook,” he said. Mr McKellar said that despite the FCAI’s conservative official industry prediction, the return private buyers and positive economic indicators including vehicle affordability should result in consistent second-half sales. “The very pleasing thing we’re seeing at the moment is that private buyers are coming back into the market in force and they’re certainly taking over the momentum that the business buyers have had for much of the past 12 months, so that’s a very positive sign. “Interest rates are certainly a factor that will influence private buyers and some of the finance figures have pulled back a little bit. (But) There’s no doubt private buyers have been back in force in May and June and if that continues we’ll get a good result for the year. “I guess the question is whether there will be any further pressure to increase interest rates between now and the end of the year. For the moment that pressure appears to have abated and new-vehicle affordability is still very much at record levels so that’s also helping underpin some of that renewed strength in private buyer activity. “We’ve upgraded our forecast so I think it’s an indication that things are moving in the right direction and I hope that will continue. There are good reasons there for optimism as we go into the second half of the year.” While sales of business vehicles were down by 16.4 per cent overall in June but remain up 10.3 per cent for the first half of 2010, sales to private buyers were up 20.8 per cent last month and continue to be up 17.5 per cent year-to-date. The strongest sales growth was seen in the SUV sector, which last month attracted 1.8 per cent fewer business buyers, but 31.4 per cent more government purchases, 33.9 per cent more private buyers and a huge 550 per cent spike in sales to rental companies. Spurred by a 28 per cent lift in business sales so far in 2010, YTD SUV sales are a massive 30.8 per cent so far this year. Business buyers deserted the other sales segments to similar degrees, but the passenger car market remains 15.8 per cent up YTD, following a 17.2 per cent increase in private buyers last month. The hitherto booming light-commercial vehicle market saw business sales reduce by a big 27.6 per cent in June but remain up 1.0 per cent YTD for a total 5.8 per cent increase in the first six months – aided by 15.3, 40.5 and 412 per cent increases in private, government and rental sales respectively in June. Toyota retains top selling position so far this year with a market share of 20.2 per cent (down from 20.7 per cent at the halfway mark of 2009), followed by Holden with 12.9 per cent (up from 12.3 per cent) and then Ford with 9.3 per cent – down from 10.2 per cent. While Ford’s market share dropped by 0.7 percentage points to 9.2 per cent in June, Holden’s grew by 0.9 to 12.7 per cent and Toyota’s fell by 1.2 points to 19.6 per cent. Other market share movers last month were Mazda (down 0.8 to 7.4 per cent), BMW (down 0.4 to 1.5 per cent), Honda (up 0.7 to 4.9 per cent), Kia (up 0.6 to 2.6 per cent) and Nissan (up 0.6 to 6.5 per cent), but in YTD terms Hyundai is the biggest improver at 8.0 per cent (up 1.4 points), while Honda remains 0.5 points down at 4.2 per cent. Niche brands Renault (down 67.2 per cent), Chrysler (down 59.9 per cent), Fiat (down 55.4 per cent) and Porsche (down 45.4 per cent) were the biggest losers last month in terms of sales, while big monthly gains were posted by Isuzu Ute (up 58 per cent), Maserati (up 50 per cent), Kia (up 39.2 per cent), Land Rover (up 38.2 per cent) and Lexus (up 43.4 per cent). YTD, the biggest sales decreases were posted by Saab, which has sold just one car all year, the discontinued Hummer brand, which still attracted five buyers last month, Dodge (down 51.8 per cent), Chrysler (down 46.9 per cent), Fiat (down 34.4 per cent) and Renault (down 31.7 per cent). Biggest YTD winners, are Isuzu Ute (up 84.2 per cent), Lamborghini (up 71.4 per cent), Jeep (up 50.8 per cent), Smart (up 48.3 per cent), Proton (up 47.4 per cent), Hyundai (up 41.5 per cent), Land Rover (up 35.3 per cent) and Mini (up 34.6 per cent). Toyota sold 21,257 vehicles in June – down 0.7 per cent but more than 7400 sales ahead of its nearest rival – and remains the only car-maker ever to sell 20,000 vehicles in a single month, thanks largely to segment leaders such as the Camry (up 35 per cent YTD), HiLux (Australia’s top-selling LCV) and Prado (which remains the nation’s top-selling medium SUV, YTD). “Sales have picked up in the mining industry and among rental fleets, while private buyers have also returned to the market, aided by improved economic conditions and strong competitive retail offers,” said Toyota’s sales and marketing chief David Buttner. YTD, Australia’s number one vehicle brand is up 14 per cent, with all models up except the Tarago (down 2.9 per cent), Aurion (down 7.4 per cent), Prius (down 15.9 per cent) and Avensis (down 29.2 per cent). Helping make up ground to the market leader for Holden was the Cruze, which posted its highest monthly sales figure to date (2987) to notch up 25,000 sales since launch. Still, the sedan-only model – which will spawn a hatch version when it goes into Adelaide production next year – trailed the best-selling small-car (Toyota’s Corolla: 4194 – up 3.1 per cent), as well as the Mazda3 (3680 – down 1.6 per cent) and Hyundai’s i30 (3209 – up 17 per cent). While the Captiva posted record monthly sales (1675 – enough to oust the Prado for top medium SUV honours in June), the Commodore had its best sales result in 12 months to remain Australia’s top-selling vehicle for the month and year, with 4679 sold in June – down 1.1 per cent on June 2009 but enough to maintain a 7.1 per cent lift YTD. Sales of the Ford Falcon were down a big 22.3 per cent in June but remain 10.4 per cent up YTD, while Toyota’s Aurion was down 20.8 per cent in June and off 7.4 per cent YTD. To June this year, Holden has sold 23,125 Commodore’s for a large-car segment share of 47.2 per cent, followed by the Falcon (16,000, 32.7 per cent) and Aurion (6102, 12.5 per cent). Holden also achieved its best June sales result for Epica and the best June since 2006 with the Barina, despite being in run-out ahead of the release of a new two-pronged model later this year. “We’re finding that Commodore and Cruze are working really well in tandem, offering buyers at both ends of the market two really compelling vehicles that make Holden the smart choice for Australian motorists,” said GM Holden sales, marketing and aftersales executive director John Elsworth. “It’s an exciting time at Holden – we’re gearing up for the launch of VE Series II Commodore later this year, and from next year, we will begin manufacturing the Cruze locally, making it the only small car made in Australia. “The market’s positive response to Cruze augurs extremely well for the success of the locally produced models in 2011,” he said. In luxury car land, while BMW had a month it would rather forget (down 15.1 per cent due to falls by all models except the run-out X5 in June), Mercedes-Benz logged its best ever sales month (2410 vehicles – up 7.9 per cent), to be up 16.7 per cent for the year. C-class sales were up 18.9 per cent last month, while the BMW 3 Series was down 41.3 per cent and Audi’s A4 was down 10.5 per cent, giving Benz a dominant 30.4 per cent share of the over $60,000 mid-size segment. Similarly, sales of the E-class boomed by 54.2 per cent in June (and by 83 per cent YTD) while its $70K-plus large-car rivals faltered, allowing the new model to join the S-class and E-class coupe/cabriolet as the leader of its segment. “The outstanding June result vindicates our price-value strategy,” said Mercedes-Benz spokesman David McCarthy. “However, our goal is not to be the number one luxury brand or even the best in each segment, but to meet our internal targets. If we meet them and we’re number one that’s just a bonus.”

Read more |

Click to shareVFACTS articlesResearch VFACTS Motor industry news GoAutoNews is Australia’s number one automotive industry journal covering the latest news, future and new model releases, market trends, industry personnel movements, and international events. |

||||||||||||||||||||||

Connect with us

Facebook Twitter Instagram