Make / Model Search

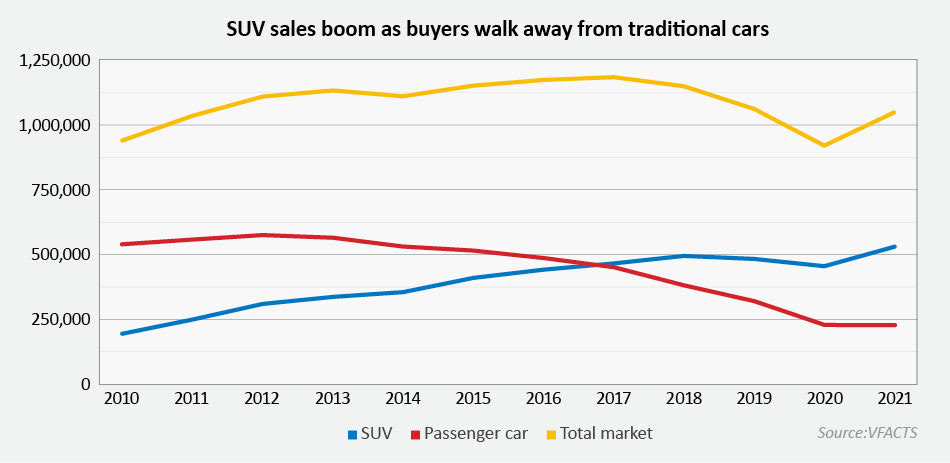

News - Market Insight - Market Insight 2022Market Insight: SUV sales soar, total market plateausMoney talks: JATO Dynamics says many European OEMs such as Peugeot are selling fewer cars than previously while reaping higher margins because SUVs like the 2008 are more profitable. More than half of Aussie market now SUVs, passenger car share slumps to 21 per centGallery Click to see larger images 17 Jan 2022 By NEIL DOWLING SUVs now account for 50.6 per cent of all new vehicles sold in Australia, a giant step on the 37.4 per cent market share on only five years ago.

The genre has added almost 91,000 annual sales between 2016 and 2021, demonstrating the huge public swell toward SUVs by the new-car buying public.

At the same time, the traditional passenger-car segment (excluding utes) has plunged a whopping 264,701 units.

Passenger cars in 2016 commanded 41.3 per cent of the total Australian new-vehicle market. Six years later, in 2021, it has shrivelled to a mere 21 per cent.

SUVs clearly have taken the market by storm – but the rise to power has come at the expense of the passenger-car segment and shows that manufacturers are generally not adding more sales but merely replacing one body style with another.

The total Australian market has retracted 8.9 per cent in the six years since 2016, crushed most recently by the effects of COVID-19 and weaker vehicle supplies.

Yet while SUV sales are up 91,000 units, passenger car sales are down 264,701, with some of the balance struck by the boom in 4x4 utes as a family vehicle, up 22.6 per cent or 42,794 units.

There are now 150 SUV models on the market in Australia and growing monthly. By comparison, in 2016 there were 119 models. The market has also introduced a new segment, the “light SUV” category which lists 17 players.

So why are there more SUVs on the market now than six years ago and why are passenger-car models slipping off the market?

Auto analyst JATO Dynamics said that in global markets, the SUV shift is all about profitability.

“With a limited number of new customers entering Europe’s new car market each year, OEMs have created new segments to attract consumer attention,” JATO said in its latest report.

“Developed in the US in the late 90s, SUVs were quickly picked up by European manufacturers and when formally introduced to the market, these vehicles soon became a real alternative to the traditional hatchbacks, wagons and MPVs that dominated Europe’s roads for decades.

“For OEMs, SUVs allowed them to enhance their model offering while charging more for vehicles that were largely identical to their hatchback equivalents.

“Consumers were, and still are, willing to pay more for an SUV than the traditional alternatives.

“For manufacturers that have struggled to hit targets over the last 10 years, they have become a welcomed revenue stream, however the surge in SUV sales has not come without negative consequences. The most significant of which has been the impact on CO2 emissions.”

JATO said the rise of the SUV has come at the cost of traditional segments.

“OEMs have worked hard to develop a wide range of SUVs, and this has directly affected the preferences of consumers, with many now considering these vehicles to be safer and generally more appealing,” it said.

“And while SUVs have helped OEM profit margins, this has had little impact on total registration volumes, which continue to plateau.”

According to JATO’s data for Europe, the seven European car brands that focused their efforts on developing SUVs have seen their overall sales in the B (light) and C (small) segments fall dramatically between 2001 and 2021.

“In 2001, the Peugeot 206 was the best-selling B-Hatch in Europe, with almost 443,000 units. At this point it was the only model offered by Peugeot within the B-segment,” said the report.

“By 2016, the 2008 joined the Peugeot line-up as its SUV counterpart to the 208 with some success. The 2008 became Europe’s second best-selling B-SUV, however, that year both models sold just 287,000 units combined, or two-thirds of the volume sold by the 206 in 2001.

“In 2021, Peugeot combined registrations did not exceed 260,000 units. Other manufacturers – including Opel/Vauxhall, Renault, and more recently Ford – have all experienced the same problem.”

JATO said that although most European OEMs are now selling fewer cars than previously, interestingly many are seeing better profit margins than they were 10 or 15 years ago.

“With the average retail price of an SUV 59 per cent higher than that of a hatchback in Europe, it is perhaps clear why sales declines across the traditional segments have not been a greater cause for concern.

Some OEMs including Volkswagen Group, BMW and Daimler, and Asian brands like Hyundai-Kia and Toyota, have capitalised on the SUV boom, increasing their market share with new products and powertrains while maintaining their position across the traditional segments.  |

Click to shareMarket Insight articlesResearch Market Insight Motor industry news GoAutoNews is Australia’s number one automotive industry journal covering the latest news, future and new model releases, market trends, industry personnel movements, and international events. |

Connect with us

Facebook Twitter Instagram